Understanding Methods and Assumptions of Depreciation

Depreciation is allocated over the useful life of an asset based on the book value of the asset originally entered in the books of accounts. Estimated useful life is the number of years of service the business expects to receive from the asset. The loss on an asset that arises from depreciation is a direct consequence of the services that the asset gives to its owner. Since the balance is closed at the end of each accounting year, the account Depreciation Expense will begin the next accounting year with a balance of $0.

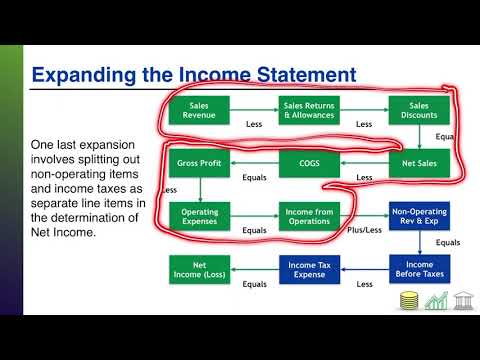

Depreciation of Long-Term Assets

It is assumed that land has an unlimited useful life; therefore, it is not depreciated, and it remains on the books at historical cost. The journal entry to record the purchase of a fixed asset (assuming that a note payable is used for financing and not a short-term account payable) is shown here. Companies have several options for depreciating the value of assets over time, in accordance with GAAP. Most companies use a single depreciation methodology for all of their assets. Thus, the methods used in calculating depreciation are typically industry-specific. The examples below demonstrate how the formula for each depreciation method would work and how the company would benefit.

Choosing Appropriate Depreciation Methods

If we want to slow down new production, extending the economic life can have the desired slowing effect. In what happens when depreciation is not added back to cash flow this course, we concentrate on financial accounting depreciation principles rather than tax depreciation. It is important to note, however, that not all long-term assets are depreciated. For example, land is not depreciated because depreciation is the allocating of the expense of an asset over its useful life.

Recording the Initial Purchase of an Asset

With this method, fixed assets depreciate more so early in life rather than evenly over their entire estimated useful life. Double declining balance depreciation is an accelerated depreciation method. Businesses use accelerated methods when dealing with assets that are more productive in their early years. The double declining balance method is often used for equipment when the units of production method is not used. Under the double-declining balance method, the book value of the trailer after three years would be $51,200 and the gain on a sale at $80,000 would be $28,800, recorded on the income statement—a large one-time boost.

It is in this sense that depreciation is considered a normal business expense and, consequently, treated in the books of account in more or less the same way as any other expense. Leasehold properties, patents, and how to set up direct deposit for employees copyrights are examples of such assets. Estimated residual value is also known as the salvage value or scrap value.

- It’s most useful where an asset’s value lies in the number of units it produces or in how much it’s used, rather than in its lifespan.

- Depreciation is listed as an expense on your income statement since it represents part of the asset cost allocated to the period.

- Track your mileage for vehicles with the mileage tracking app, organize your assets to measure depreciation, and make tax season a breeze with automated financial report generation.

- One often-overlooked benefit of properly recognizing depreciation in your financial statements is that the calculation can help you plan for and manage your business’s cash requirements.

In addition, there is a loss of $8,000 recorded on the income statement because only $65,000 was received for the old trailer when its book value was $73,000. Sometimes, these are combined into a single line such as ”PP&E net of depreciation.” These assets are often described as depreciable assets, fixed assets, plant assets, productive assets, tangible assets, capital assets, and constructed assets. A depreciation schedule is a schedule that measures the decline in the value of a fixed asset over its usable life. This helps you track where you are in the depreciation process and how much of the asset’s value remains. Because you’ve taken the time to determine the useful life of your equipment for depreciation purposes, you can make an educated assumption about when the business will need to purchase new equipment.

Understanding depreciation helps you predict the value of your asset and claim the relevant tax deductions to reduce your total taxable income. As with the straight-line example, the asset could be used for more than what is balance sheet reconciliation five years, with depreciation recalculated at the end of year five using the double-declining balance method. When analyzing depreciation, accountants are required to make a supportable estimate of an asset’s useful life and its salvage value. It is difficult to determine an accurate fair value for long-lived assets.

Why Are Assets Depreciated Over Time?

Also, depreciation expense is merely a book entry and represents a ”non-cash” expense. The market value of the asset may increase or decrease during the useful life of the asset. However, the allocation of depreciation in each accounting period continues on the basis of the book value without regard to such temporary changes. The expenditure on the purchase of machinery is not regarded as part of the cost of the period; instead, it is shown as an asset in the balance sheet. Suppose that the company changes salvage value from $10,000 to $17,000 after three years, but keeps the original 10-year lifetime. With a book value of $73,000, there is now only $56,000 left to depreciate over seven years, or $8,000 per year.